Latest1 week ago

Latest1 week agoAPC plotting to frustrate Peter Obi’s 2027 ambition — Obidient Movement

Crime1 week ago

Crime1 week agoEaster tragedy: Gunmen storm churches in Kaduna, kill seven, abduct worshippers

Latest6 days ago

Latest6 days agoThird ADC faction surfaces, Norman Obinna claims leadership, dismisses rival groups

Business1 week ago

Business1 week agoSpiro expands electric mobility in Ogun State with 1,000 new bikes

Latest6 days ago

Latest6 days agoAtiku affirms loyalty to ADC, expresses confidence in Court ruling on David Mark’s leadership

Crime1 week ago

Crime1 week agoBenue Easter horror: 17 dead, several missing, homes razed in Mbalom community attack

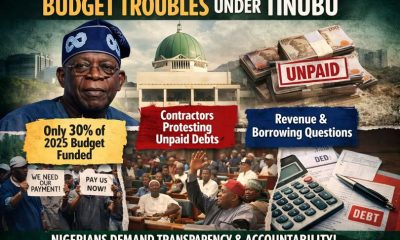

Business1 week ago

Business1 week agoNigeria faces growing debt risks as 2026 borrowing jumps to N29.2trn

Football6 days ago

Football6 days agoOpta SuperComputer backs Arsenal for historic UEFA Champions League triumph