Featured

Nigeria’s rising debt sparks debate despite subsidy removal

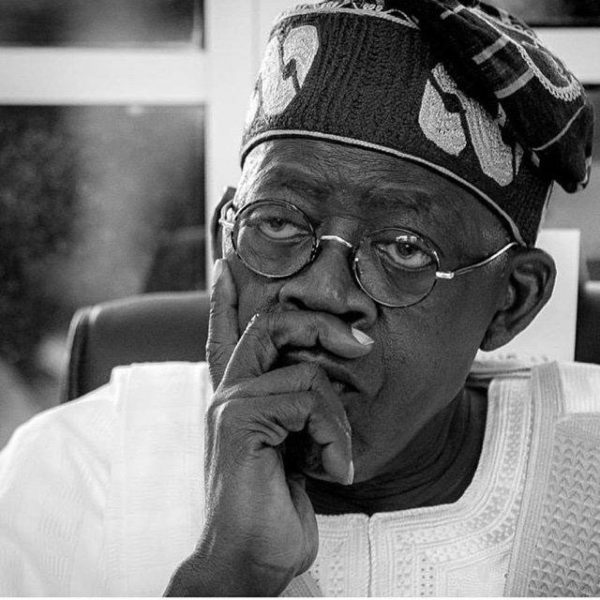

Nigeria’s debt burden has reached a new milestone just as President Bola Tinubu has sought fresh Senate approval for a $516.3 million foreign loan to finance sections of the 1,000-kilometre Sokoto–Badagry Superhighway, a flagship infrastructure project that has intensified a national debate over the country’s borrowing trajectory, fiscal sustainability, and whether subsidy savings are truly delivering for ordinary Nigerians.

Data released on April 14, 2026, by the Debt Management Office (DMO) showed that Nigeria’s total public debt climbed to ₦159.28 trillion by the end of December 2025, a year-on-year increase of ₦14.61 trillion or 10.1 percent from ₦144.67 trillion in December 2024. The figure means every Nigerian now carries an average debt load of ₦66,250.

The Tinubu administration’s borrowing has been markedly faster than that of its predecessor. Under President Tinubu, from May 2023 to September 2025, public debt rose by roughly $45 billion or ₦66 trillion in just over two years, averaging about $20 billion annually. By comparison, the previous Buhari administration added roughly $52 billion over eight years, or about $6.5 billion per year on average.

In a letter to Senate President Godswill Akpabio read during Thursday’s plenary session, President Tinubu formally requested Senate approval for a $516,333,070 syndicated loan from Deutsche Bank to fund Sections 1, 1A, and 1B of the Sokoto–Badagry Superhighway — approximately 120 kilometres of the total 1,000-kilometre corridor.

The President described the highway as a flagship project under his Renewed Hope Agenda, designed to link Sokoto, Kebbi, Niger, Kwara, Oyo, Ogun, and Lagos states from Illela to Badagry, opening up Nigeria’s Northwest–Southwest economic corridor. The project is expected to cut logistics costs, reduce travel time, improve road safety, enhance trade and food security, and strengthen national integration by linking production zones to ports and markets.

The loan will be supported by a partial risk guarantee from the Islamic Corporation for the Insurance of Investment and Export Credit (ICIEC), while the Federal Government is required to contribute ₦265.5 billion as counterpart funding for land acquisition, compensation, and related works. The Senate President referred the request to the Senate Committee on Local and Foreign Debts, directing it to report back within one week.

The highway request is part of a larger borrowing surge. On March 31, 2026, President Tinubu had separately asked the National Assembly to approve external loans totalling $6 billion — including a $5 billion structured financing from First Abu Dhabi Bank for budget support and debt servicing, and $1 billion from Citi Bank/UK Export Finance for Lagos port rehabilitation. The National Assembly approved both requests the same day.

The central paradox driving public disquiet is that the removal of petrol subsidies in May 2023 hailed at the time as a transformational reform that would free up tens of billions of dollars annually has not translated into visible fiscal relief. Instead, the savings appear to have been swallowed by debt servicing costs.

Independent assessments by the Nigerian Economic Summit Group (NESG) show that Nigeria’s debt-service-to-revenue ratio rose to 116.8 percent in 2024 and remained critically high at approximately 113 percent in the first quarter of 2025. Analysts warn that a debt-service-to-revenue ratio approaching or exceeding 100 percent is widely regarded as fiscally unsustainable.

Official data from the 2026–2028 Medium-Term Expenditure Framework show that between January and July 2025, the government earned ₦13.67 trillion in revenue falling far short of the prorated target of ₦23.85 trillion, representing a shortfall of ₦10.19 trillion or 42.7 percent. For those months, debt servicing and salaries combined gulped 105 percent of all government earnings.

The numbers have prompted sharp warnings from economists and financial experts.

David Adonri, Vice Executive Chairman of Highcap Securities, accused the government of being “addicted to debt,” arguing that “despite subsidy removals and claims of higher revenue, public spending keeps expanding.” He described the oil revenue benchmarks in the 2025 budget as “aggressive and unrealistic,” noting that actual production has averaged around 1.6 to 1.7 million barrels per day while prices have dropped to around $65 per barrel far below the budgeted assumptions.

Tunde Abidoye, Head of Research at FBNQuest Merchant Bank, echoed similar concerns, warning that “with OMO yields above 20 percent and the Monetary Policy Rate at 27.5 percent, debt servicing costs are rising faster than revenues. This approach offers short-term fiscal relief but worsens long-term vulnerabilities.”

One fiscal analyst, Ayinde, pointed to what he described as a credibility gap between the government’s public claims and available data: “Either selective metrics are being used, or the underlying fiscal position has not improved to the extent publicly represented.”

The Federal Government has consistently defended its borrowing as both necessary and constitutionally sound. DMO Director-General Patience Oniha, speaking at the IMF Spring Meetings in Washington, stressed that Nigeria’s borrowing process is tightly controlled, noting that every loan, domestic or external must secure National Assembly approval before it is contracted, with detailed public hearings that build investor confidence by signalling strict compliance with the law.

The DMO has also clarified that a significant portion of the apparent debt surge under the Tinubu administration reflects the depreciation of the naira, which substantially increased the local currency value of existing external loans, rather than solely new borrowing.

Analysts at Daily Trust noted that recent fiscal reforms, including foreign exchange unification, subsidy removal, tighter tax enforcement, and improved liquidity, have reduced the debt-service-to-revenue ratio to 65 percent by early 2025 — down from a peak of 162 percent in 2024 — though independent assessments dispute this figure.

The debt-to-GDP ratio has remained relatively moderate in official projections, estimated at around 34.7 to 39 percent for 2026 depending on GDP rebasing. However, analysts warn that optimistic assumptions mask underlying vulnerabilities, especially with persistent deficits and high servicing costs.

For millions of Nigerians grappling with inflation, rising transport costs, and shrinking purchasing power, the numbers carry a personal weight that transcends fiscal policy debates. Nigeria’s 2025 budget included a debt servicing allocation representing approximately 25 percent of total spending — raising concerns among economic analysts about its impact on expenditure in health, education, and social welfare.

While the government maintains that the debt-to-GDP ratio remains within globally acceptable limits, analysts warn that the debt-to-revenue ratio — one of the highest in Africa — poses a more urgent challenge that GDP benchmarks alone fail to capture.

With the 2027 general election cycle now looming, the pressure on the Tinubu administration to show that borrowing for mega-projects like the Sokoto–Badagry Superhighway is translating into tangible improvements in Nigerians’ daily lives is only set to intensify.

Energy1 week ago

Energy1 week agoFuel price surge deepens economic pressure across Nigeria

Aviation1 week ago

Aviation1 week agoEight killed in helicopter crash on Indonesia’s Borneo Island

Energy1 week ago

Energy1 week agoOil prices slide as U.S., Iran announce reopening of Strait of Hormuz after Lebanon ceasefire

Health1 week ago

Health1 week agoNewly released emails show NIH scientist feared job loss after questioning COVID-19 vaccine mandates

Agribusiness6 days ago

Agribusiness6 days agoHealth experts raise alarm over antibiotic residues in poultry products in Nigeria

Sports7 days ago

Sports7 days agoUsyk backs Joshua to defeat Fury as heavyweight rivals train together in Spain

Trending Stories7 days ago

Trending Stories7 days agoBakery sues TikToker for ₦50m over viral ‘Everlasting Bread’ claim

Energy1 week ago

Energy1 week agoDangote Refinery plans Pan-African IPO to drive $40b expansion