Business

Nigerian Economy: From First to Fourth in Africa

The report, a few days ago, by one of the Bretton Woods institutions—the International Monetary Fund (IMF)—that Nigeria now ranks the fourth largest economy in Africa is a shocker to not a few observers. The IMF in its latest ‘World Economic Outlook’ estimates Nigeria’s gross domestic product (GDP) at US$252 billion based on current prices, lagging behind Algeria at US$267 billion, Egypt at US$348 billion, and South Africa at US$373 billion.

Nigeria which has held the title of “Africa’s largest economy” since 2013, after rebasing her GDP, is now projected to remain in the fourth place for years to come. Following the rebasing in 2013, Nigeria’s GDP hit US$510 billion, and was projected to reach US$1 trillion in ten years’ time (i.e. 2023); against this expectation, however, the country’s GDP shrank almost by half to stand at US$252 billion at end-2023, according to the IMF’s estimates.

The IMF further says Africa’s most industrialised nation (South Africa) would remain the continent’s largest economy until Egypt reclaims the mantle in 2027. According to the IMF’s projection, Nigeria is expected to remain in fourth place for years. “Nigeria and Egypt’s fortunes have dimmed as they deal with high inflation and a currency plunge,” the report said.

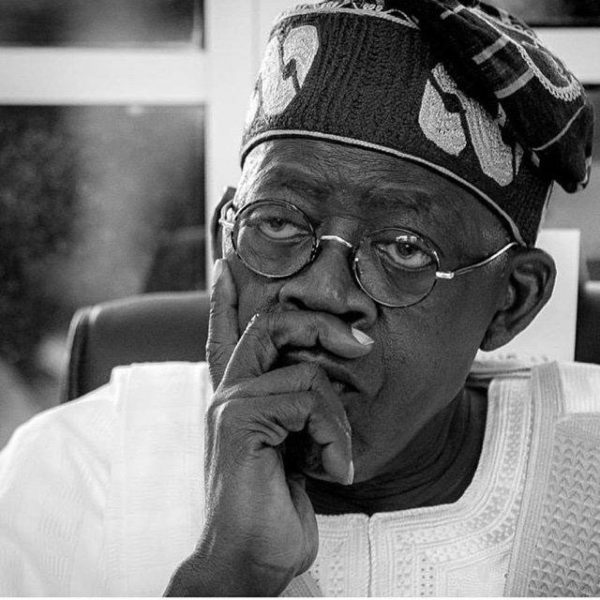

The IMF says without mincing words that Nigeria’s drop from its premier position as “Africa’s largest economy” is as a result of the reforms, policies and programmes of the Nigerian government in recent years. For instance, President Bola Ahmed Tinubu-administration announced the floating of the naira in June last year and the scrapping costly opaque energy and fuel subsidies in the face of dollar shortages.

Over the years, no doubt, Nigeria’s national currency, the Naira, has been losing strength against the US dollar and other hard currencies, the rate at which it depreciated since the June 2023 amounted to a crash. From less than N500/US$1 in May 2023, the exchange rate crashed to nearly N200/US$ in February/March 2023, before coming down to about N1200/US$ in April. The exchange rate has however maintained high volatility—and by the third week of April, the Naira has been getting weaker—losing value against the dollar. Indeed, as of April 24, the Naira was exchanging at N1300/US—with the likelihood of even losing more strength against the dollar.

As the Nigerian currency has kept losing strength in the Forex (or FX) market, the rate of inflation has also been going sky-high. From about 21 per cent early in 2023, the rate of inflation (Consumer Price Index, CPI) had hit 33.20 per cent as at end-March 2024. Again, this runaway inflation trend has been largely partially policy-induced and partly structural. As a largely import-dependent economy, Nigeria’s import value and volume are usually huge; this implies deployment of so much FX to importation of several item—including machineries and raw materials.

This very high cost of imported items (especially raw materials and other intermediate goods) usually get ‘transferred’ to the ultimate consumers—and manifests as rising inflation via the ‘cost-push’ mechanism. On the other hand, the structural challenge of dilapidated road network and poor infrastructure –all combine to hike the cost of production and distribution of goods and services across Nigeria. This generally uncompetitive business environment has seen not a few multinationals and other blue chips leaving the country in droves in recent times.

Still on the structural front, Nigeria’s economy has been hamstrung by its almost sole dependence on oil exports, leaving it vulnerable to price shocks in global energy markets. Indeed, recent policies such as fuel subsidy removal by the Tinubu administration exposed the country to total dependence on imported petrol (Premium Motor Spirit)—leaving hitherto functioning refineries to remain moribund. This not only led to skyrocketing prices of the PMS at the pump, but also led to sharp rise in the prices of virtually all goods and services via high cost of transportation.

The Nigerian, too, economy has been rightly dubbed a “generator economy”—because every economic agent—individuals, households, businesses and government agencies—mainly depend on generating sets for their power supply. The public power supply has remained epileptic—and keeps getting worse—even after so-called privatization. For businesses, getting whatever approvals and/or certifications is also usually a harrowing experience—essentially because of the very high level of corruption and unnecessary red-tape entrenched in the officialdom.

In the face of all these, Nigerians’ high taste or preference for foreign goods and services has consistently messed up efforts by successive administrations at meaningful economic diversification. Neither the political will nor patriotic public support has truly underlined the use of “made in Nigeria.” Economy diversification, for several years has remained a mere mantra or slogan or propaganda in the hands of government officials. The inflow of petro-dollar in the past five decades or so, has left Nigeria only a consuming nation—mere rentier economy—and people with high propensity for spending/consumption.

Unsurprisingly, the sitting President Tinubu administration has not remarkably effected any changes; instead, pervasive corruption and poor governance have further undermined any progress and permeated public institutions. Decades of plunder and misallocation of resources by successive administrations have left Nigeria with decrepit infrastructure in dire need of upgrading. Basic services like electricity, transportation, and internet connectivity are worrisomely unreliable. The costs and inefficiencies imposed on businesses operating in this environment have constrained private enterprise and deterred long-term investments and inflow of Foreign Direct Investments (FDIs).

The accumulated rot and virtual collapse of Nigeria’s economic substructure till date constitute the impediment to the nation’s economic progress. And this is why although some of the President Tinubu policies could be taken as well-intentioned as part of a broader economic liberalisation drive, these policies have worsened near-term pains and sufferings for the Nigerian public. The Naira has plunged significantly against the dollar—remaining on a tailspin and practically collapsing the country’s dollar-denominated GDP output. Subsidy removals (for PMS) and hiking of electricity tariff have caused domestic prices for food and fuel to spike sharply against a backdrop of mounting global and domestic inflationary pressures.

The consequences of this economic quagmire, both immediate and longer-term, remain dire. In the near-term, Nigeria’s GDP measured in U.S dollar terms has fallen from around $477 billion in 2022 to an estimated $253 billion for 2024 based on current projections. This devaluation-induced GDP shrinking has enabled economies like South Africa, Egypt and even Algeria to surpass Nigeria in the GDP rankings by the IMF and others.

For a country with such lofty aspirations of regional leadership and pre-eminence, the import of the IMF’s projection of relinquishing its status as Africa’s biggest economy cannot be overstated. Nigeria’s global standing has diminished, too, as have its capacity to project power and shape continental affairs. More tangibly, its dropping economic fortunes has also dampened foreign investment sentiment, with investors adopting a wait-and-see attitude to see whether Nigeria economy can emerge from the woods.

The longer-term outlook is even more precarious if this economic malaise persists. Nigeria has suffered cyclical booms and busts in the past due to its hydrocarbon-dependent nature. But this time around, the stagnation comes superimposed on an already dire situation of widespread poverty, high double-digit inflation, decrepit infrastructure, decaying public services and heightened insecurity that has turned an existential threat. The subsisting social unrest and internal displacement have since triggered a vicious cycle of wide-spread economic disruptions and enduring capital flight.

Now, with the Tinubu administration seemingly at its wits end, and deeply engaged in policy somersaults, it is becoming increasingly real that it will take a while for Nigeria’s economy to make it out of the abyss. The recent resort to the setting up of several layers of economic management teams and committees, further gives credence to the administration’s search for a straw to cling onto while in the puddle. All said, the onus is that of Nigeria to prove the IMF’s projections wrong. There is no alternative!

- The author, Okeke, a practising Economist, Business Strategist, Sustainability expert and ex-Chief Economist of Zenith Bank Plc, lives in Lekki, Lagos. He can be reached via: [email protected]

-

Education5 days ago

Education5 days agoUniversity of Ibadan releases 2026/2027 post-UTME screening results

-

Football5 days ago

Football5 days agoUnpaid £185m Club World Cup fund sparks fresh FIFA controversy

-

Business7 days ago

Business7 days agoInformation Minister, VON DG to lead ARCON’s 2026 Advertising Industry Colloquium

-

Aviation6 days ago

Aviation6 days agoCanada issues 10 key tips to help immigration applicants avoid processing delays

-

Business1 week ago

Business1 week agoCooking gas dealers slash prices amid intensifying market competition

-

Business4 days ago

Business4 days agoBreaking: NNPCL reduces pump price of petrol as competition intensifies

-

Politics1 week ago

Politics1 week agoKenneth Okonkwo questions INEC’s credibility, calls for reforms ahead of 2027 polls

-

Latest6 days ago

Latest6 days agoFubara’s early push for political structure triggered rift – Wike