Business

Can Interest Rate Hikes Curb High Inflation in Nigeria?

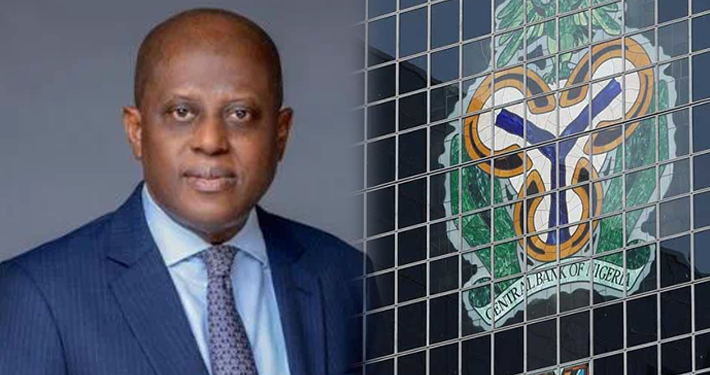

The question: ‘Can the Central Bank of Nigeria (CBN) curb the high and rising inflation in the country with endless hiking of Monetary Policy Rate (MPR)?’is most germane, given what has been going on in the monetary space in the country since February 2024. For three consecutive times during its monetary policy committee (MPC) meetings (in February, March and May), the apex bank has raised the MPR by an unprecedented total of 750 basis points: from 18.75% to 26.25%. Each hike of the MPR, according to the CBN, is in the effort to rein in soaring inflation.

The headline inflation rate in Nigeria has assumed a runaway dimension; rising steadily in the past one year, from 22.22% in April 2023 to 33.69% in April 2024—the highest level in about three decades. Incidentally, the latest MPR (26.25%) fixed by the MPC on May 21, 2024, has turned (arguably) the highest level in Nigeria’s monetary policy rate history. Before now, the highest MPR was 26% in 1993, when inflation rate was 61.26%, according to National Bureau of Statistics (NBS) data.

Notably, the runaway inflation rate trend is essentially driven by soaring prices of food in the country. In other words, food inflation is at the core of the persisting high inflation rate in Nigeria. Lamenting this in the MPC communique (May 21, 2024), chairman of the committee and Governor, CBN, Olayemi Cardoso, said the MPC “reiterated several challenges confronting the effective moderation of food inflation to include rising cost of transportation of farm produce; infrastructure-related constraints along the line of distribution network; security challenges in some food-producing areas; and exchange rate pass-through to domestic prices for imported food items.”

Continuing, the “MPC urged that more be done to address the security of farming communities to guarantee improved food production in these areas.” The communique said “members further observed the recent volatility in the foreign exchange market, attributing this to seasonal demand, a reflection of the interplay between demand and supply in a freely functioning market system.”

It needs be pointed out, however, that the persistent hike in MPR as adopted by the CBN, poses potential and real dangers to the growth of the economy. In truth, rising inflation is not entirely a monetary phenomenon; and so, the solution to it is not fully within the domain of monetary authorities. Now, with the MPR at 26.25%, effective lending rates by deposit money banks (DMBs) will fall between 35-40%–and which genuine business would borrow at these rates, and thrive? The new MPR is therefore not pro-business!

Also, with Cash Reserve Ratio (CRR) standing at 45%, again, the highest in a very long while, it means that the DMBs will be leaving almost fifty percent of their deposits (‘sterilized’) at the CBN per time. Thus, in the bid by the CBN to fight runaway inflation (‘single-handedly’), the DMBs’ capacity to create credit (lending capacity) will be seriously restrained/constrained or curtailed.

On the other hand, as pointed out by Mr. Cardoso, none of the factors responsible for the surge in the prices of foodstuff and related items in the high inflationary trajectory is within the control of the apex bank. The rising cost of transportation is entirely within the upshots of fuel subsidy removal a year ago, May 29, 2023. Nigeria has since then depended on almost one hundred percent import of petrol (Petroleum Motor Spirit, PMS) for all local needs. No local refinery as of today is known to be providing even a litre of PMS in the market.

Following from this, so much foreign exchange (FX) deployed to importing the PMS translates to rising ‘landing cost’ for the product; and is passed on as high pump price of PMS. This translates to persistent rise in cost of transportation for all economic agents, including the farmers. And the CBN is in no position to refine crude oil or to import PMS, or to assist the farmers with transportation logistics to get their produce to the market. In point of fact, the rapid depreciation of the Naira in the Forex (FX) market has since led to the Nigerian National Petroleum Company (NNPC) Limited being left as the ‘sole’ importer of the PMS.

The upshot of this is that Independent Petroleum Marketers have become mere ‘price takers,’ a situation that has led to ‘avoidable scarcity’ and continued rise in the prices of PMS. Thus, for several months running, there has been scarcity of the product in various parts of the country—with prices ranging from N600 to N750 per litre. Unfortunately, the Dangote Refinery that is expected to begin to refine and supply PMS locally, will be importing much of its crude oil requirement from the United States (US).

A report by Bloomberg says Dangote Refinery would buy at least 24 million barrels of US crude over the next year “as it ramps up its processing capabilities.” The report says the Refinery has issued a term tender for the purchase of two million barrels a month of West Texas Intermediate (WTI) crude for 12 months starting in July 2024. With Dangote Refinery which is located in the export processing zone in Lagos also importing its crude from the US, it is very doubtful if it would be selling its product (PMS) cheap to Nigerians. Really it is very unlikely that Dangote’s products would crash the prices of PMS; and so, lower the cost of transportation any soon.

Indeed, in reality, Dangote Refinery has recently increased the price of its diesel per litre, in response to further Naira depreciation in the FX market. Same would most likely apply to PMS when available from the Dangote plant. While this will be playing out, the negative effect of widespread insecurity in Nigeria on farming, farmers and food supply cannot be overemphasized. Although the MPC communique blamed food shortage on “security challenges in some food-producing areas”, insecurity in Nigeria more pervasive and has since become an existential threat.

Not only that numerous farmers have been displaced from their farms/villages by armed bandits and vagrants, most of them are now quartered in Internally Displaced Persons (IDPs) camps across the country. This same insecurity also constitutes a major repellent to many local investments as well as inflow of the much-needed Foreign Direct Investment (FDI). All the blue chip companies that have been exiting Nigeria in recent months, without exception, blamed insecurity and generally bleak economic climate for leaving the country. What can the CBN do in this regard?

The CBN was also not saying the whole truth when the MPC said “the recent volatility in the foreign exchange market was due to seasonal demand.” The point truly is that the apex bank has not yet got it right in terms of insufficiency of FX supply in the forex market. Although the CBN’s recent efforts yielded some ‘hot money’ from Foreign Portfolio Investors (FPIs) and Diaspora remittances, these are not yet much and sustainable inflows to deal effectively with the acute FX shortage of the forex market.

Ironically, while the CBN is enthroning tight monetary stance in fighting inflation, its fiscal authority counterpart is taking an expansionary posture. This is why cost of governance keeps ballooning by the day; monthly FAAC money allocation to the three tiers of government is now in trillions; and the Federal Government remains on borrowing binge. Trillions of Naira is being squandered through all manner of ‘palliatives’ by all tiers of government; there are so-called ‘salary awards’, and elevated minimum wage that must come into place in no time! All these are inflation drivers, and are largely beyond the purview of the apex bank.

- The author, Okeke, a practising Economist, Business Strategist, Sustainability expert and ex-Chief Economist of Zenith Bank Plc, lives in Lekki, Lagos. He can be reached via: [email protected] (08033075697 SMS only)

-

Education5 days ago

Education5 days agoUniversity of Ibadan releases 2026/2027 post-UTME screening results

-

Football5 days ago

Football5 days agoUnpaid £185m Club World Cup fund sparks fresh FIFA controversy

-

Business7 days ago

Business7 days agoInformation Minister, VON DG to lead ARCON’s 2026 Advertising Industry Colloquium

-

Aviation6 days ago

Aviation6 days agoCanada issues 10 key tips to help immigration applicants avoid processing delays

-

Business1 week ago

Business1 week agoCooking gas dealers slash prices amid intensifying market competition

-

Business5 days ago

Business5 days agoBreaking: NNPCL reduces pump price of petrol as competition intensifies

-

Politics1 week ago

Politics1 week agoKenneth Okonkwo questions INEC’s credibility, calls for reforms ahead of 2027 polls

-

Latest6 days ago

Latest6 days agoFubara’s early push for political structure triggered rift – Wike